Sandi Martin

Sandi Martin

June's list of the best Canadian personal finance news, articles, and blog posts from around the internet, expertly curated for interest and relevance

Source: https://blog.springpersonalfinance.com

"In the short run, however, the best way [for financial journalists] to get ahead is to check your conscience at the door. Most readers, and all too many editors, want to hear about the newest, the hottest, the get-rich-quick schemes, the secret “keys to wealth” that have miraculously been overlooked or hidden by “the experts.” Good advice easily gets drowned out by advice that just sounds good."

Yet another reminder to be careful about your financial news consumption: "There is a perfect inverse correlation between how much you care about the opinions of others and how serious you are about managing money"

Some of the most brilliant people I’ve met are terrible investors because they’re constantly seeking out ways to explain why things happen the way they do in the markets.

This is it: the post to read about why and how to read financial news.

TL;DR ruthlessly curate your sources of financial news to stop yourself from believing that you can see patterns that don't exist.

"Your results should come not from anticipating changes in the financial markets, but from avoiding changes in your own plan."

Unless someone has a sensible explanation and good data to document a strategy’s returns–both before and after it was created–you’re dealing with investment hogwash

If you ever wanted proof that money coaching worked, and that financial planning is for people at all stages of life (not just those with investing questions), here it is.

In an interview earlier this week I was asked a great question about the counter-intuitive nature of investing. The question was basically, "How can investors learn to swallow their pride to earn satisfactory, but above average returns while giving up on the chance to earn extraordinary returns?"

There are countless lazy articles on the Internet about how to save more money, 99.9% of which are detached from reality. Everyday I get emails from readers that say things like: "I want to travel / quit my job/ retire in 10 years. But I don't have the savings."

Retirement income planning has emerged as a distinct field in the financial services profession. And while it suffers from many growing pains as it gains recognition, increased research and brainpower in the field have benefited retirees and those planning for retirement. One matter has become even clearer than before: The financial circumstances facing retirees differ dramatically from pre-retirees.

The trouble with evaluating the success or failure of an asset allocation model over a short period of time - or in real-time - is that one of the primary benefits to the strategy involves non-correlated assets - and correlations aren't constant.

"I’m a big believer in focusing on what you control as a form of risk management. While we’re never going to be able to perfectly measure risk, one of the best ways to manage risk is to have a comprehensive plan in place. Having a plan doesn’t mean you can eliminate risk altogether. That’s impossible. Taking risk makes sense. You just don’t want to get into the habit or taking unnecessary or unacceptable risks."

By reading a fund’s lengthy prospectus and entering the documented, yet buried, sales fees (load), management fees (MER), and other fees (such as account set-up and redemption fees) into a Mutual Fund Fee Calculator, I can not-so-easily show my friends how simple it is to get confused by how much they’re paying to invest in mutual funds.

Financial literacy leader Jane Rooney led a year-long consultation with Canadians to devise a strategy for improving our money management skills. The strategy, unveiled this week, will equip people to achieve their key goals in three areas: (1) Controlling spending and debt. (2) Planning and saving for the future.

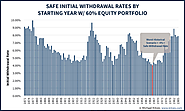

While the 4% rule was created as a means to set a minimum income floor – a spending amount low enough that, even if “bad” things happen, the withdrawals will be low enough to be sustainable until/as the market recovers – that doesn’t mean spending can never be raised. After all, a few years into retirement, it should be clear whether that adverse sequence-of-return-risk event has or has not occurred.

The Star featured a story last week of a family in a tight situation: they had bought a pre-construction house, which was delayed by several years and had shrunk from the sales model. They decided to cancel the deal and get their deposit back, which led to trouble of one sort.

The Globe's Rob Carrick speaks with financial planner Sandi Martin about the services a financial planner provides

Fee only/advice only financial planner at Spring Financial Planning, ex-banker, curmudgeon.

Co-host with the really loud laugh on Because Money