Sandi Martin

Sandi Martin

July's list of the best Canadian personal finance news, articles, and blog posts from around the internet, expertly curated for interest and relevance. You can follow this list right here in List.ly, by following me on Twitter (@sandimartinspf), or by signing up for Spring in your inbox here: https://springpersonalfinance.com/contact/

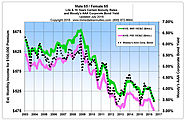

"With such slim prospective returns on offer, you will have to lower your expectations and raise the amount you save.

“Investing is always a partnership between you and the markets,” says Mr. Kinniry. In the 1980s and 1990s, when stocks and bonds alike racked up double-digit average returns, the markets did most of the work. “But now you are going to have to be the majority partner,” he says.

In this weird world, if you want to have more money, you will need to save a lot more money."

"deals and rewards are only truly frugal when they’re applied to a budgeted-for purchase that was already going to happen"

"Making presumptions about who’ll pay for what is mighty shaky ground on which to start a new life"

"He spent his money on his own priorities. Who says it must be better if he went to law school, made $330k a year, and retired at 33 to travel the world on a $24,000/year budget"

"recovering from bear market losses while you are still working, earning income, and buying stocks at discounted prices is one thing. Recovering those losses after you start spending in retirement using stocks that have fallen in value and having no income to buy discounted stocks is quite another."

What Scottish poet Andrew Lang said of politicians--that they "use statistics in the same way that a drunk uses lampposts"--could also be said of the Investment Funds Institute of Canada's (IFIC) recent effort to illustrate the value investors receive from paying mutual fund fees.

If you keep hearing about "CRM2", here's the best set of explanations I've found. You owe it to yourself to watch them.

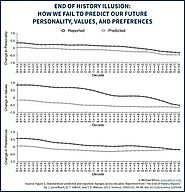

"In the face of uncertainty about spending, investment returns, interest rates, the housing market, inflation, and your own health and longevity, the uncomfortable truth is that you have to pick your poison. You can protect yourself against some risks, even optimize your plans for some set of probable outcomes, but you can’t avoid every risk and optimize for every outcome."

"In this context, it’s more about doing financial planning to understand what goals would be possible, rather than pursuing any one in particular, and ensure that goals aren’t so risky that no (tolerable portfolio could achieve them). And planning strategies like “avoid or minimize debt” become highly relevant, not because “debt is bad” but simply because “debt limits choices” and reduces flexibility… in a world where, as noted, we can’t really predict what we’ll like and want to do in the future. Similarly, “emergency savings” isn’t just about having available cash for an “emergency”, but any number of significant life choice changes, from getting married to having kids to getting divorced, or going back to school or changing jobs or starting a business."

I always get asked about 0% financing on auto loans, and whether or not they can make sense from a planning perspective even if you have the means to pay cash for a car. I get the thinking, with the opportunity cost, etc. But it always comes as a surprise to people to learn that 0% financing may end up having higher costs than you realize.

June's list of the best Canadian personal finance news, articles, and blog posts from around the internet, expertly curated for interest and relevance.

Fee only/advice only financial planner at Spring Financial Planning, ex-banker, curmudgeon.

Co-host with the really loud laugh on Because Money

![[Video] How 0% financing can actually cost you more money | Preet Banerjee](http://media.list.ly/production/280711/1804551/item1804551_185px.jpeg?ver=5278136622)